USD was the best-performing currency amidst a modest week in volatility. Stronger manufacturing activity and industrial production reinforced the resilience of the US economy. It's been resilient of late and, overall, in the past few months, relative to its peers.

Although the latest Fed rate was unchanged, it somehow really boosted the currency. Other top-performing currencies were the Aussie and the yen, while those that faltered included the likes of NZD and GBP.

We didn't see any specific fundamental data for these performances. However, the yen is also similarly robust as the dollar from an economic perspective.

What moved the forex market this week?

There was a string of interest rate decisions this week, the outcomes of which panned out as expected. The Bank of Japan boosted its figure by 0.25%. Although this didn't provide a notable boost to the currency, JPY has recently benefitted from improving business investment and an offset from external trade.

USD certainly stole the show on Wednesday. Despite an unchanged interest rate, the dollar has accumulated lots of smaller positive surprises across labour, inflation, and growth. So, this was likely one of the main contributors to its rising prices.

What could move the forex market next week?

The US dollar dominates the calendar this week, with several high-impact releases covering inflation, growth, employment and consumer spending. The Australian dollar, euro, and Canadian dollar all have important inflation-related data, while the Japanese yen could remain active due to several Bank of Japan speeches.

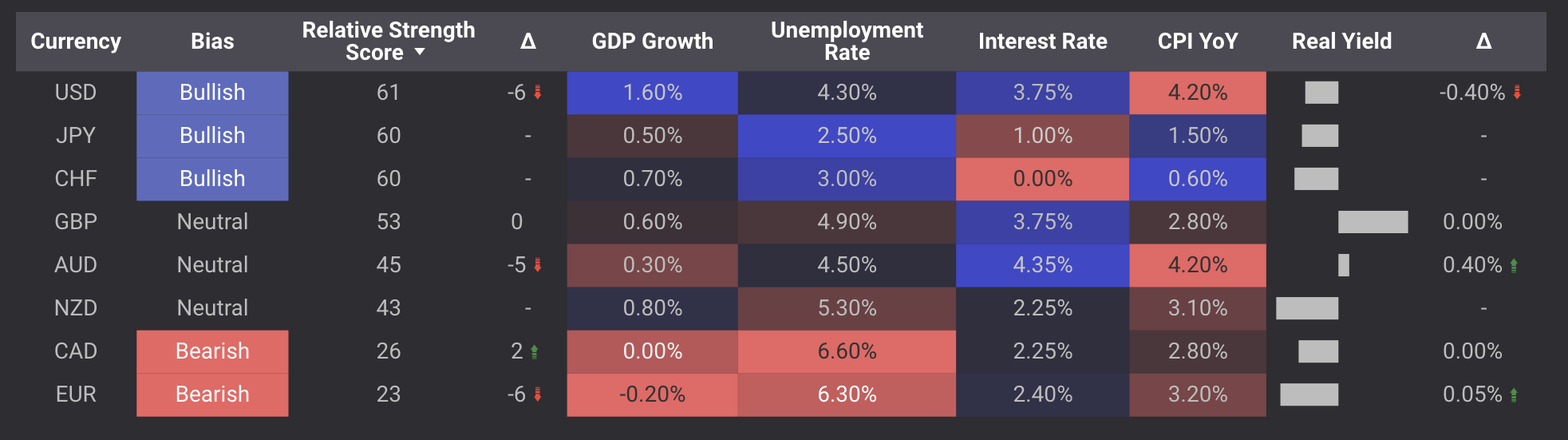

Let's explore the currencies with the biggest potential catalysts. Below are two images (the Eco Surprise and Eco Strength indices from Edgefinder) that provide an overview of how the respective economies compare.

USD – Plenty of Opportunities to Extend Momentum

The US has by far the busiest calendar this week, although Thursday is the standout. Traders should pay close attention to the final GDP reading, Core PCE inflation, Personal Spending, and Initial Jobless Claims. Most of the forecasts suggest the US economy remains in relatively solid shape. GDP growth is expected to be revised higher from 0.5% to 1.6%, while Personal Income and Personal Spending are also forecast to improve. Core PCE inflation, however, is expected to remain unchanged, suggesting that underlying price pressures remain persistent.

Another week of potentially positive economic surprises could provide fresh support. That said, with so many releases scheduled, the greenback could experience increased volatility throughout the week.

AUD – Could Gain if Inflation and Jobs Surprise Higher

Australia has a fairly important calendar outside the United States. Wednesday's monthly inflation figures are followed by Thursday's employment report, giving traders two major opportunities to reassess expectations for the Reserve Bank of Australia. Headline inflation is expected to rise from 4.2% to 4.4%, while trimmed mean inflation is also forecast to edge higher. If these estimates are exceeded, markets could become more optimistic about future RBA policy.

The labour market is also expected to improve, with the Employment Change forecast to rebound to 30,000 after the previous decline and the unemployment rate projected to fall slightly to 4.4%. These forecasts could help reinforce some bullish sentiment. However, disappointing inflation or employment data would quickly weaken that outlook.

EUR – Modest Upside Possible if Business Confidence Continues Improving

Several PMI readings are expected to improve modestly, particularly within France's services sector and Germany's composite index. Germany's Ifo Business Climate is also forecast to rise slightly, suggesting business confidence may be stabilising after recent weakness. These releases should provide a clearer picture of whether economic activity across the eurozone is beginning to recover. If the Eco Surprise Index already points to improving momentum, stronger-than-expected PMIs could give the euro an additional boost. Otherwise, another round of disappointing surveys may reinforce concerns about sluggish growth.

CAD – Inflation Will Take Centre Stage

Canada's biggest release arrives early in the week with the latest inflation report. Headline CPI is expected to increase from 2.8% to 2.9%, while both monthly and core inflation measures are also forecast to edge higher. Since inflation remains one of the Bank of Canada's primary concerns, these figures could influence expectations for future monetary policy. If inflation surprises to the upside, the Canadian dollar may receive additional support. However, a weaker-than-expected report would likely reduce expectations for tighter policy and could weigh on the currency.

JPY – Hawkish BOJ Signals Could Lift the Yen Further

Japan has a relatively lighter economic calendar, but several speeches from Bank of Japan officials could still generate volatility. Traders will be looking for any clues regarding future interest rate increases or the Bank's broader policy outlook. Meanwhile, the latest PMI surveys present mixed expectations, with services activity expected to improve slightly while manufacturing is forecast to soften.

If the Eco Surprise Index continues to rank the yen among the stronger-performing currencies, any hawkish comments from Bank of Japan officials could help extend that momentum. Conversely, cautious guidance may limit further gains despite the currency's recent economic strength.

Conclusion

The currencies we have highlighted are those with the best chance of some action. However, you are always free to analyse other pairs in the vast forex market. For a granular look at the most impactful events in the forex economic calendar, read our article here.